Problem set for graduate students to price European options using the binomial model and calculate delta-hedging portfolios.

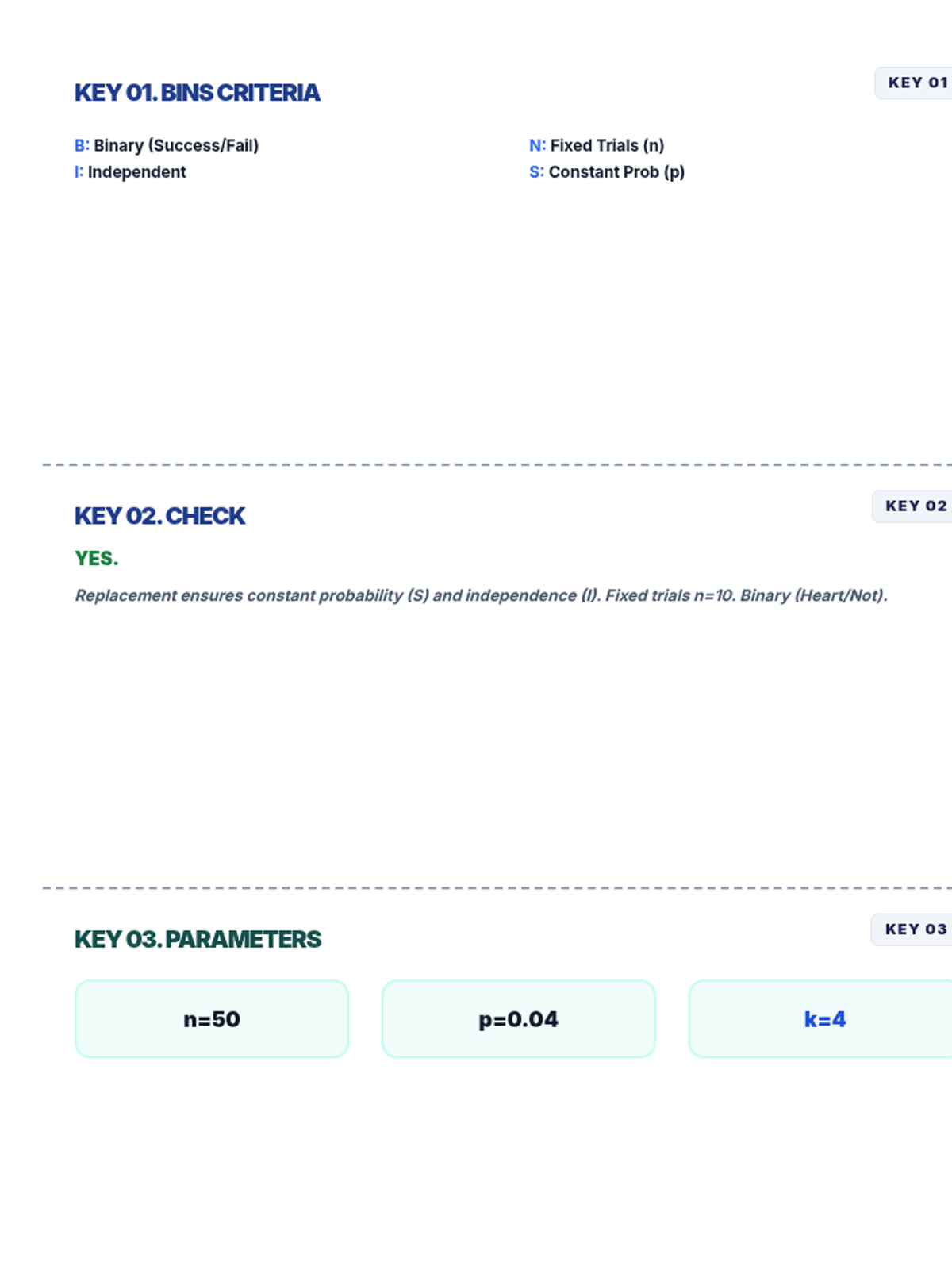

A comprehensive answer key for the Binomial Blitz Quiz, featuring detailed explanations, manual formula rendering, and logic breakthroughs for the assessment questions.

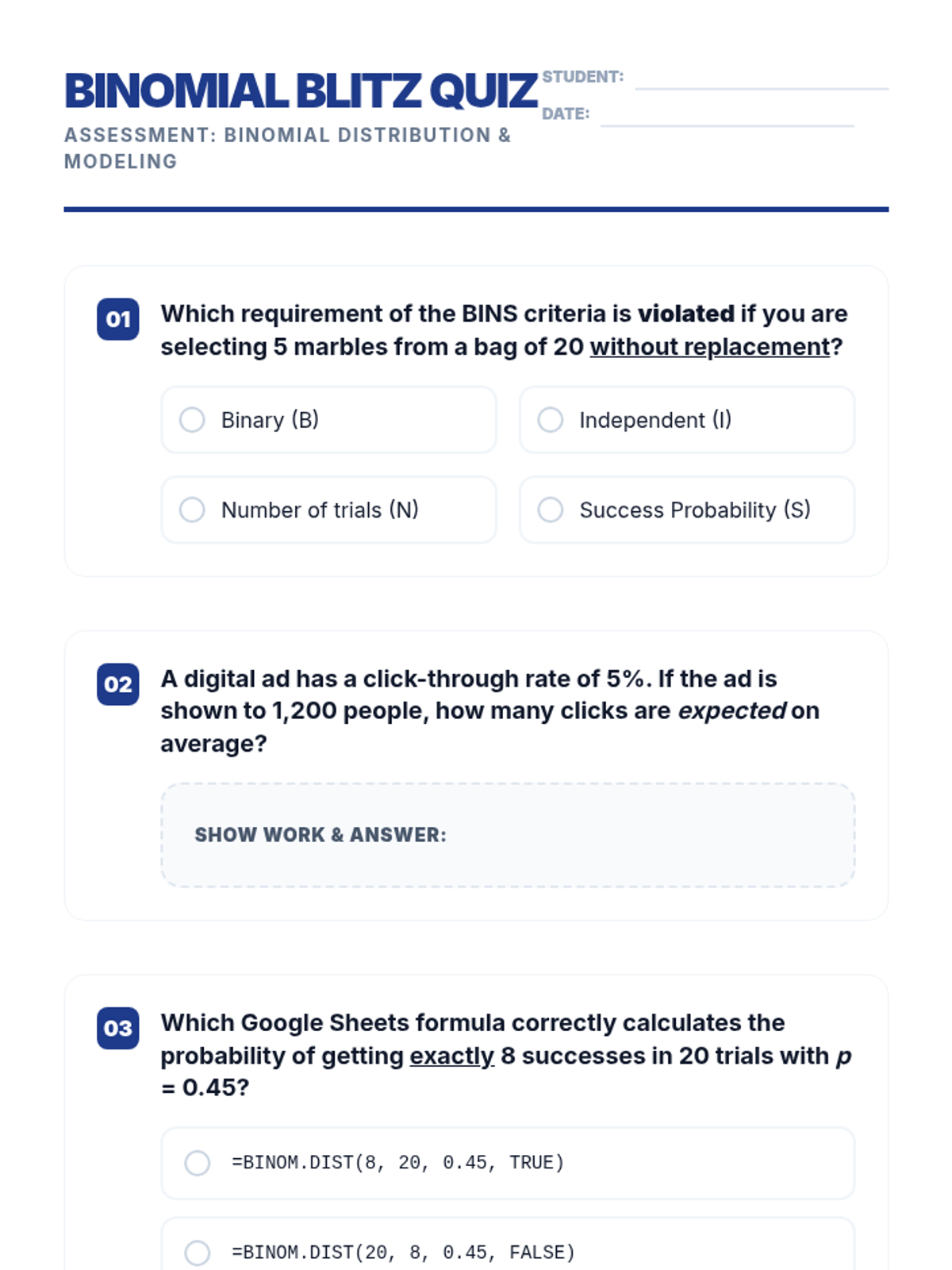

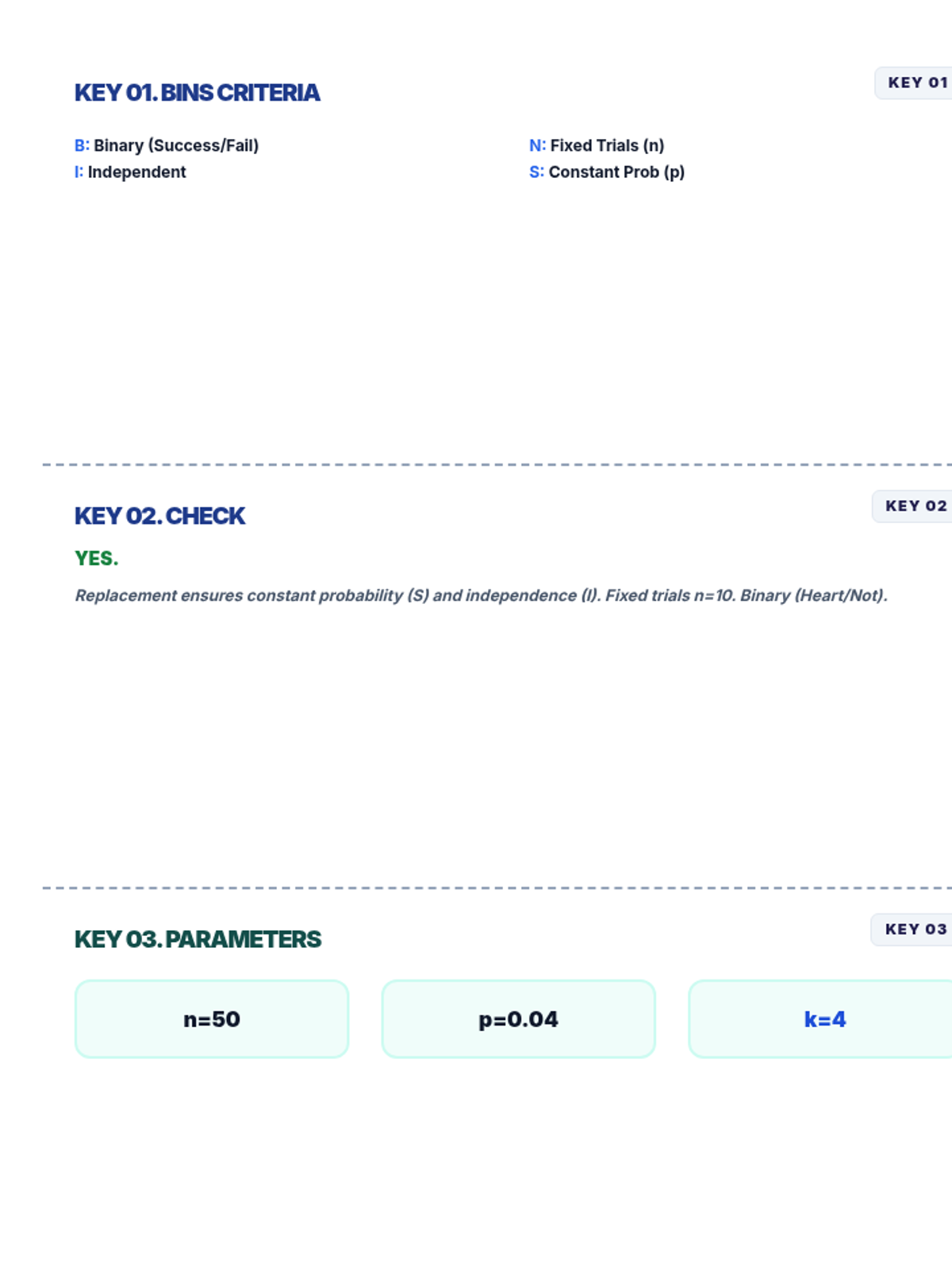

A 10-question assessment covering the BINS criteria, binomial parameters, spreadsheet formula syntax, hand-calculation theory, and expected value. Designed for 12th-grade statistics with high-quality visual formatting and clear student work areas. Updated with fixed math rendering and page break protections.

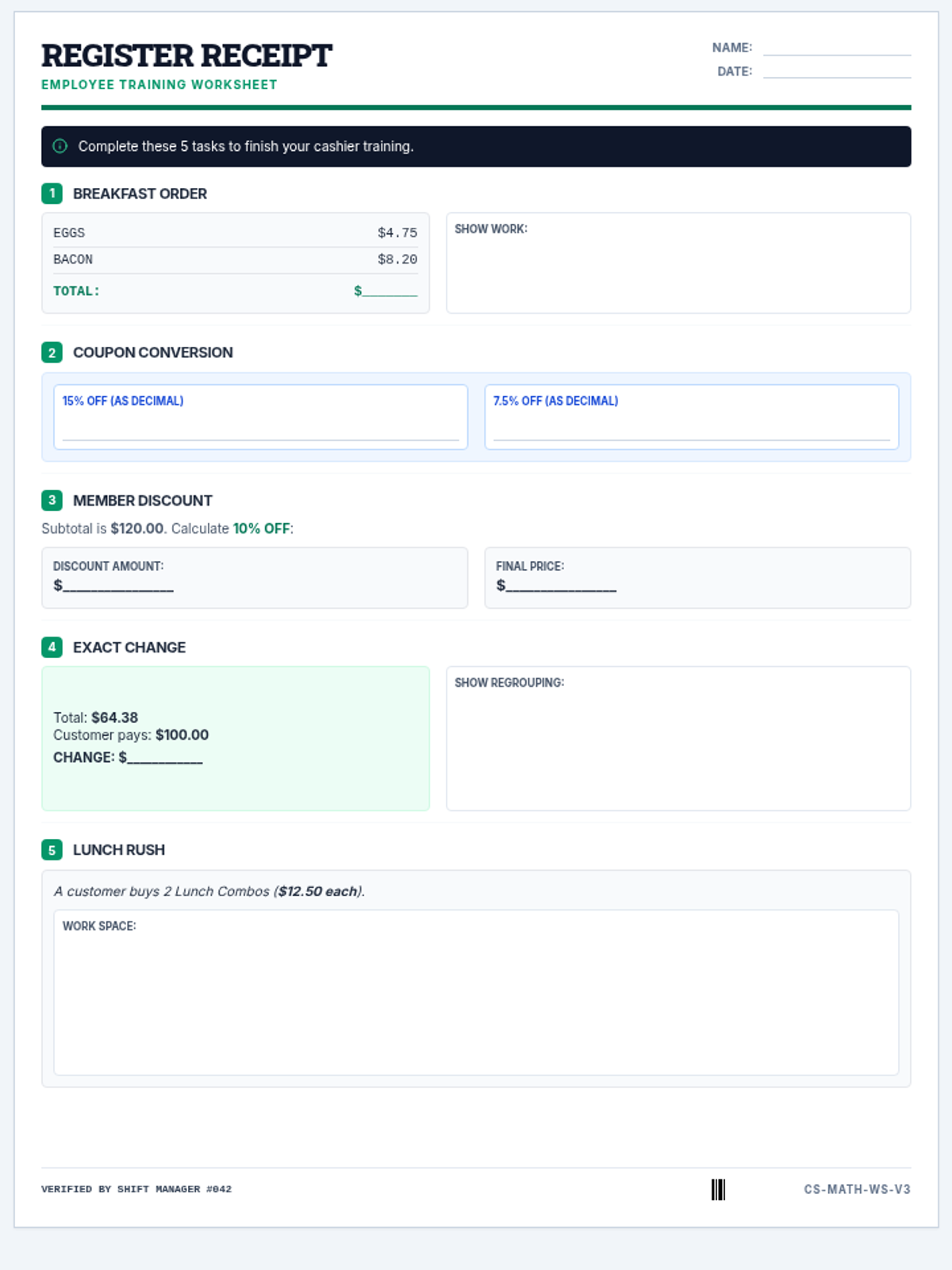

A student-facing worksheet for practicing retail arithmetic, including multi-item totals, percentage discounts, and complex change-making with regrouping. Updated to fit all 5 problems on one page with high-contrast footer.

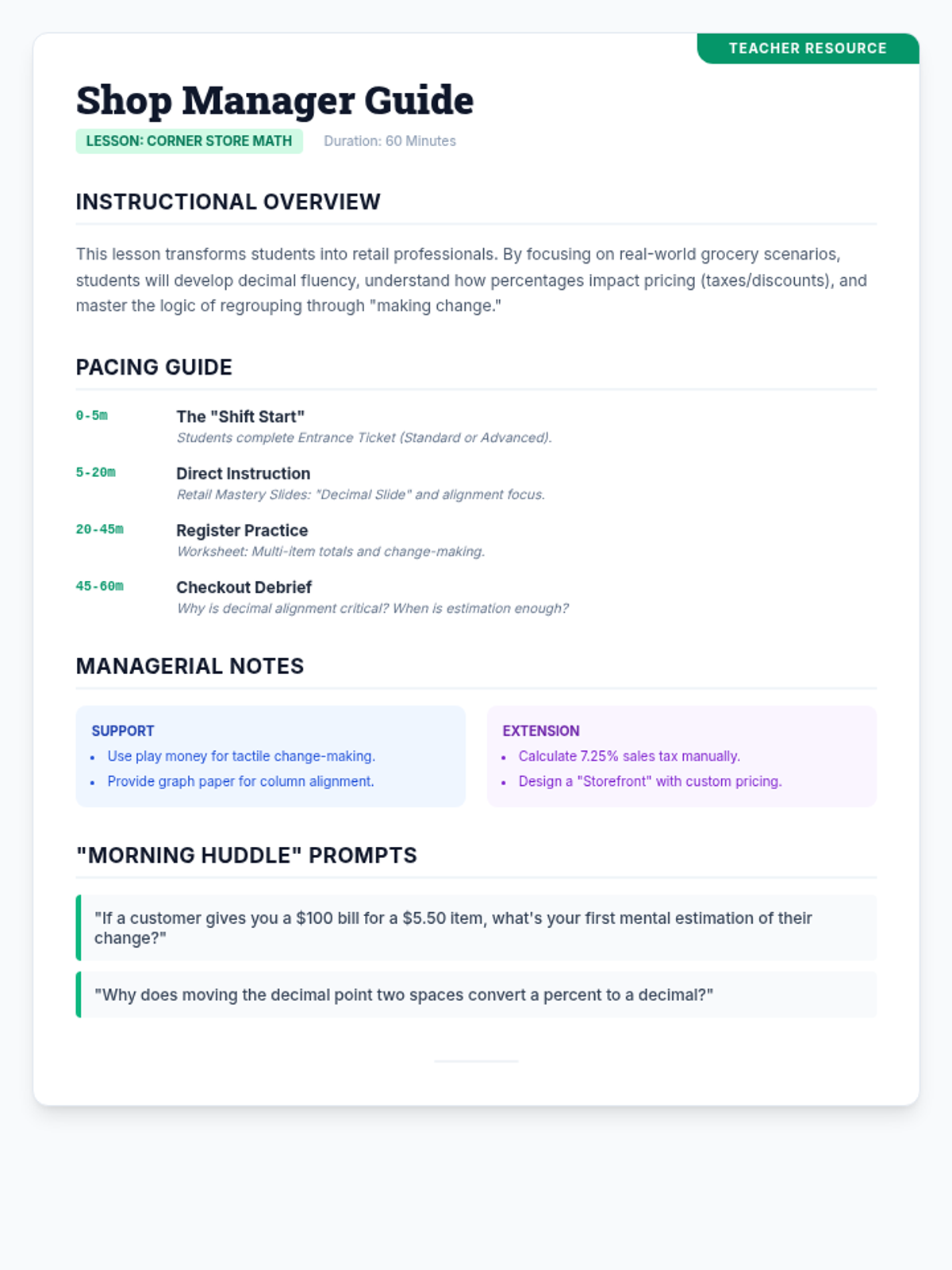

A teacher's facilitation guide for the Corner Store Math lesson, including pacing, differentiation strategies, and discussion prompts. Updated for better page fit.

An instructional presentation for teaching retail math, covering decimal alignment, percentage conversions, and mental math strategies for checkout scenarios. Updated with 5 problems.

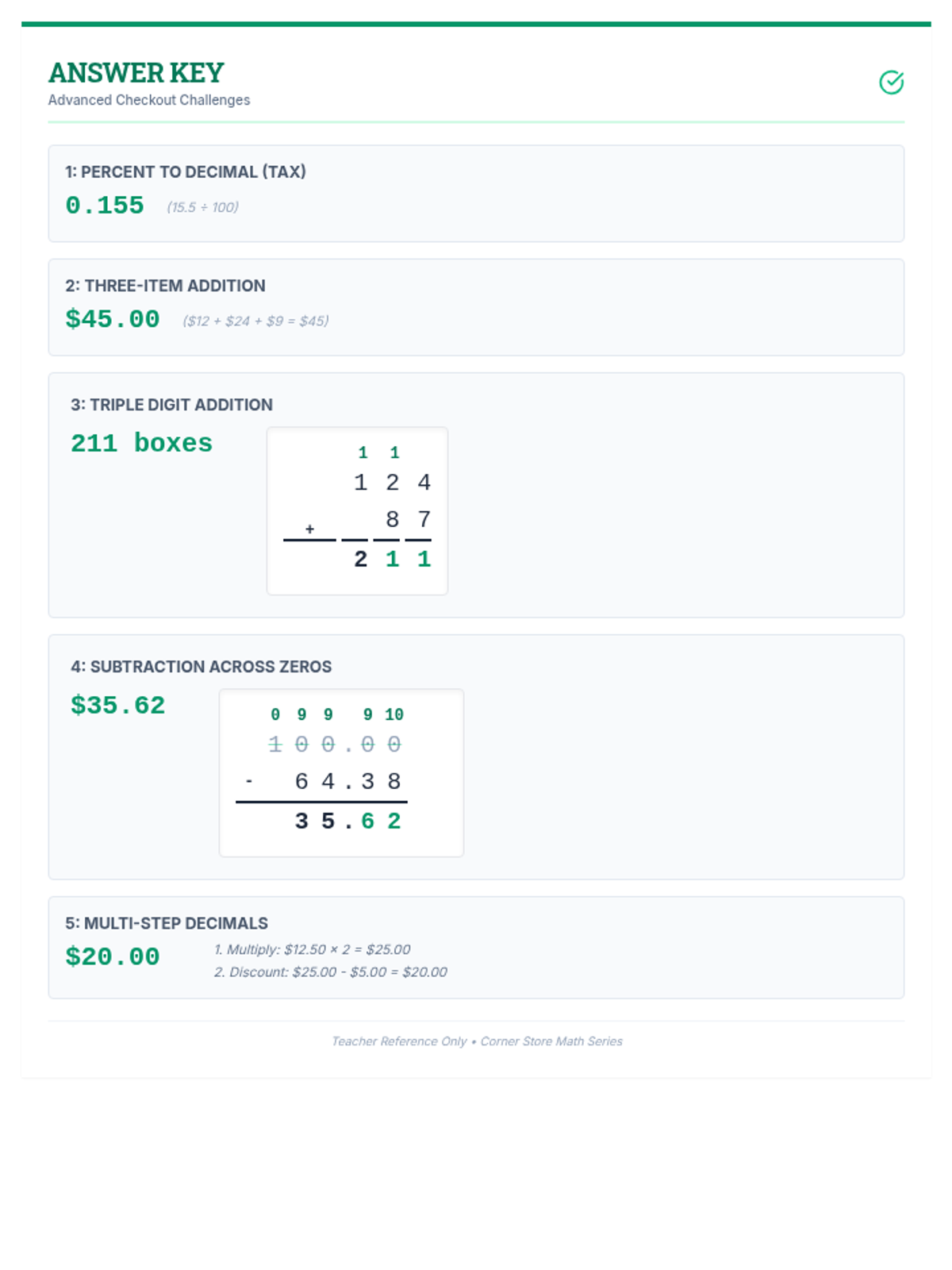

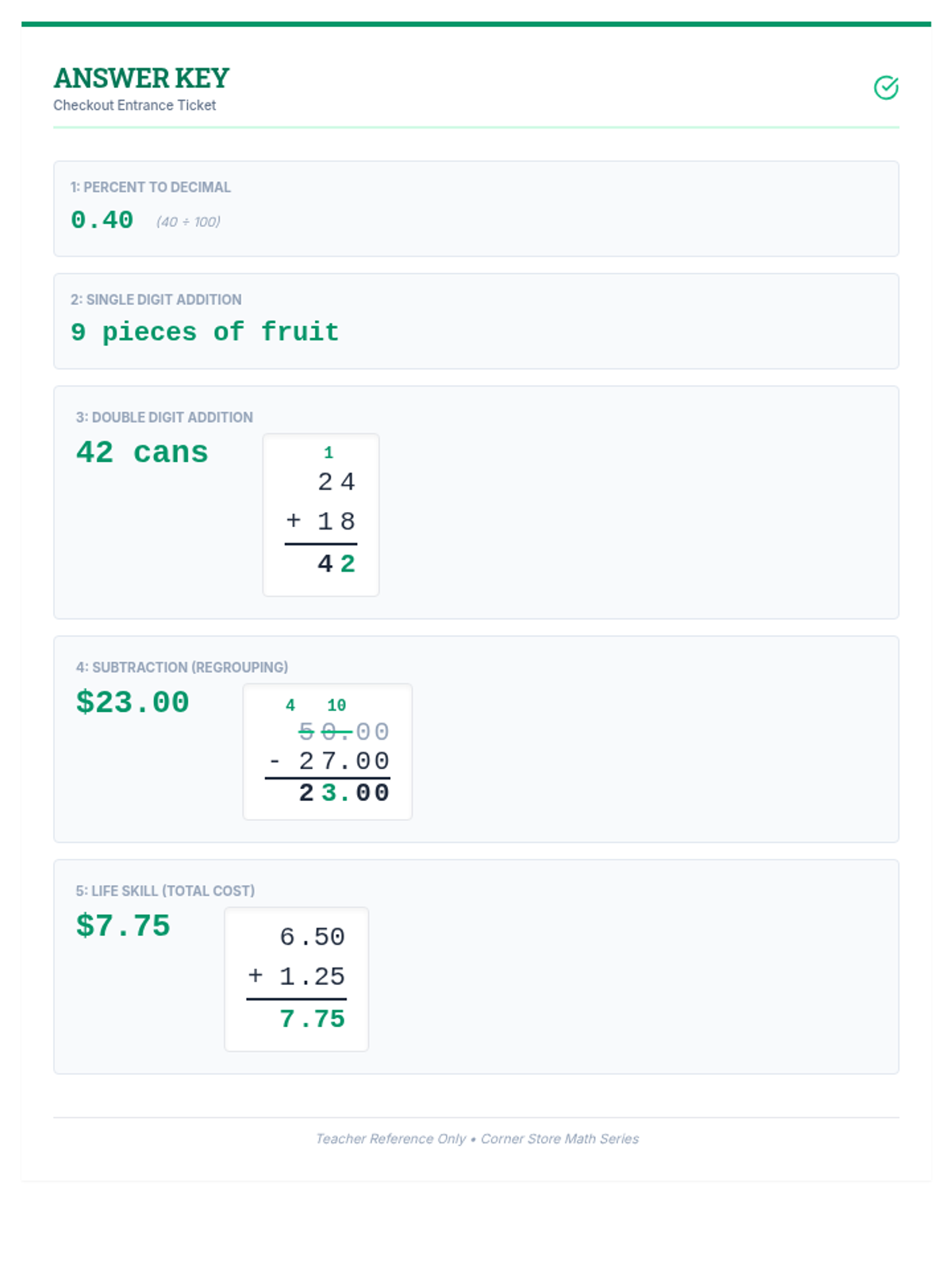

Answer key for the advanced entrance ticket, featuring step-by-step solutions for subtraction across zeros and multi-step decimal problems. Visuals updated for better alignment.

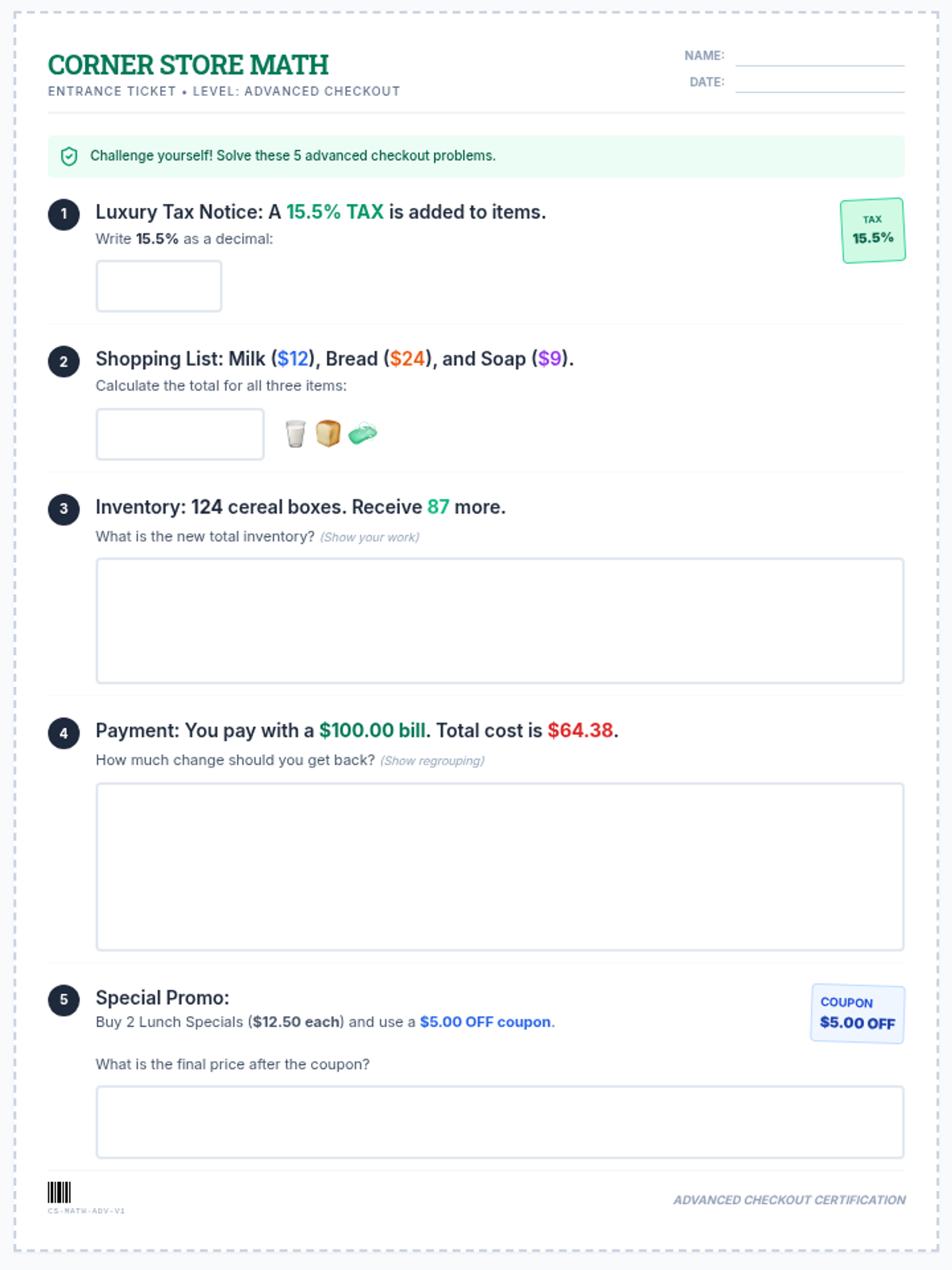

An advanced version of the grocery-themed entrance ticket featuring more complex multi-digit addition, subtraction across zeros, and multi-step decimal problems.

An answer key for the Checkout Entrance Ticket, providing solutions and step-by-step regrouping explanations. Visuals aligned for clarity.

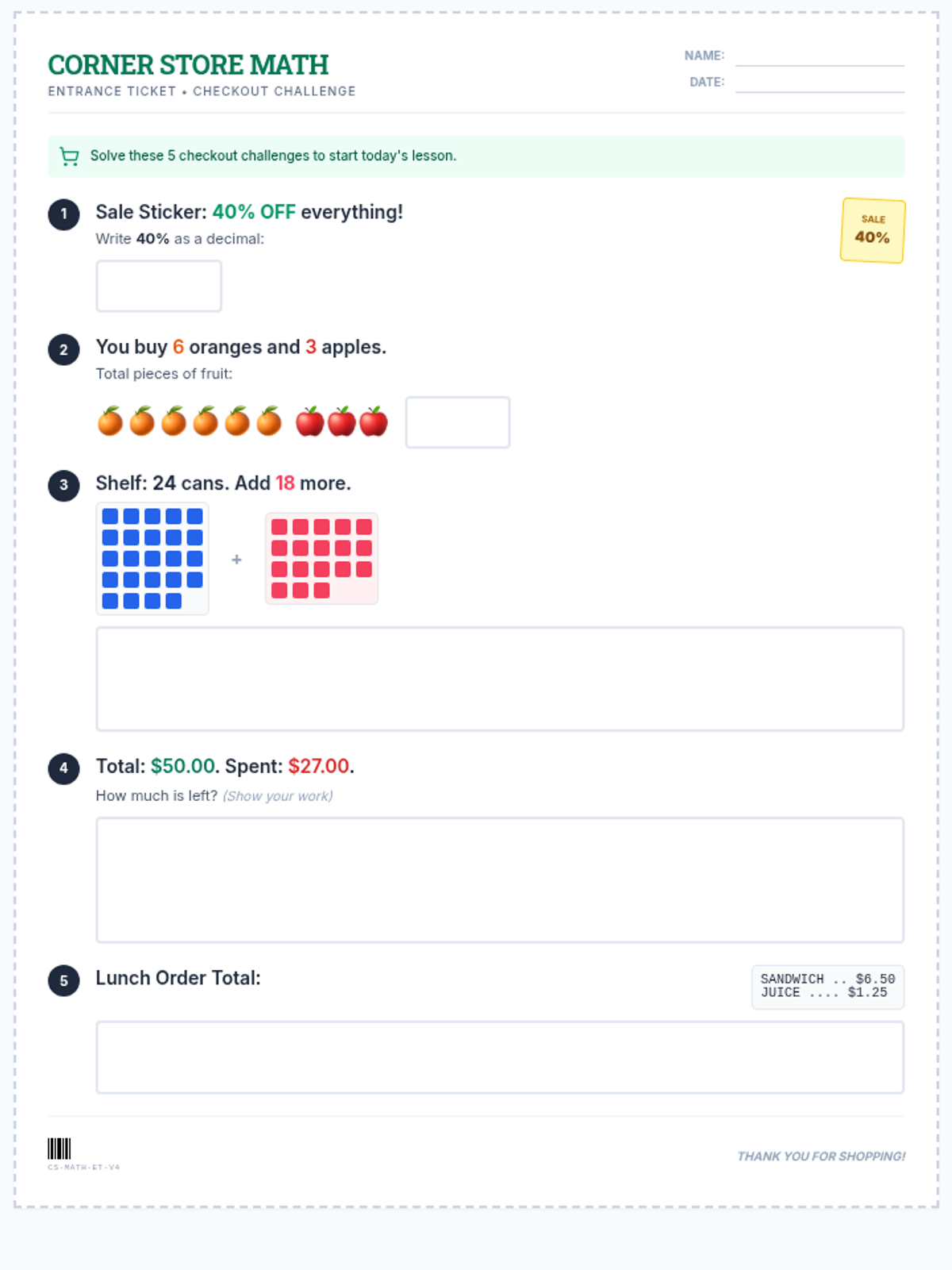

A grocery-themed entrance ticket covering percentages, basic addition/subtraction, regrouping, and money-based life skills with visual aids. Updated for better page fit.

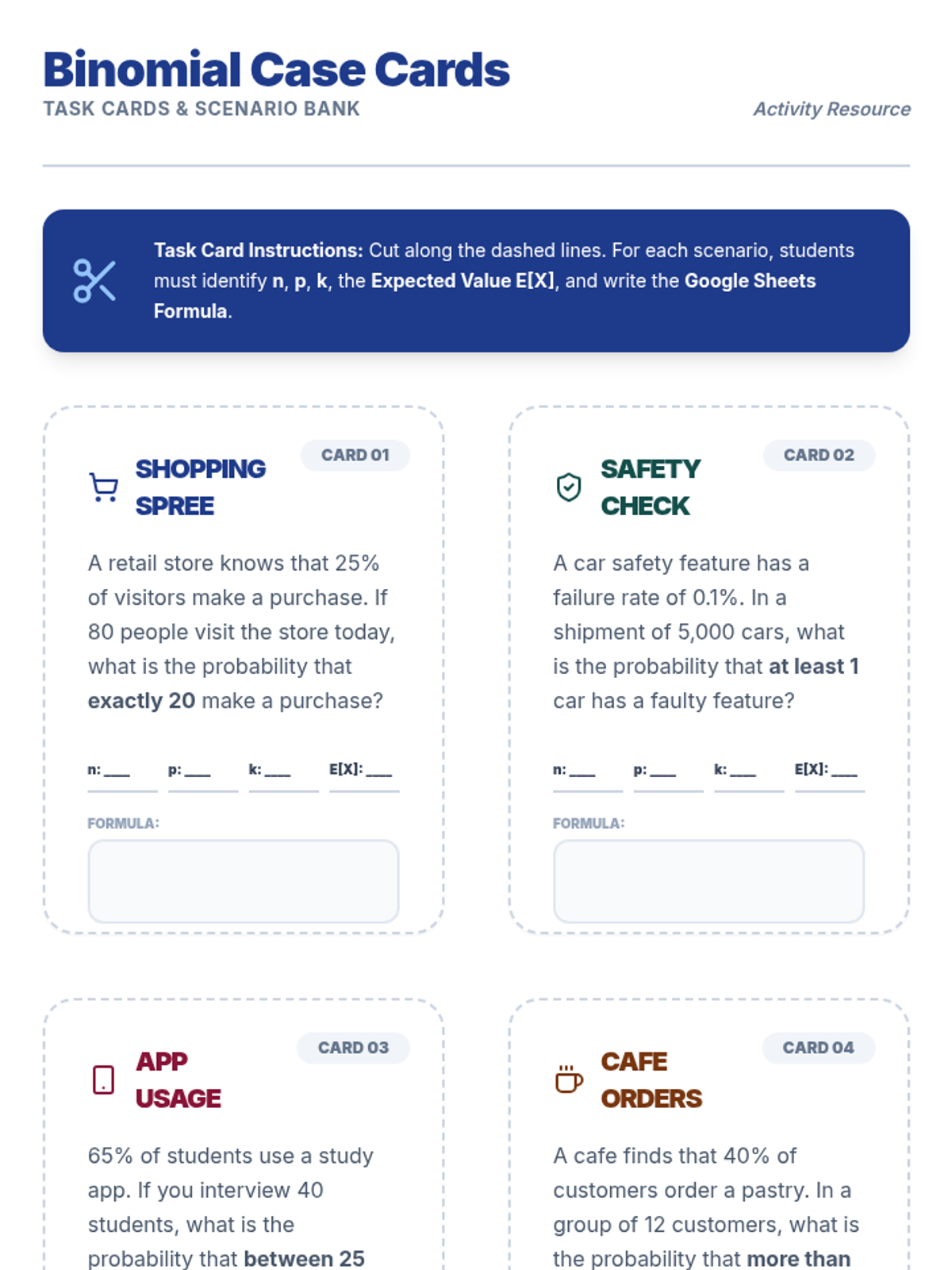

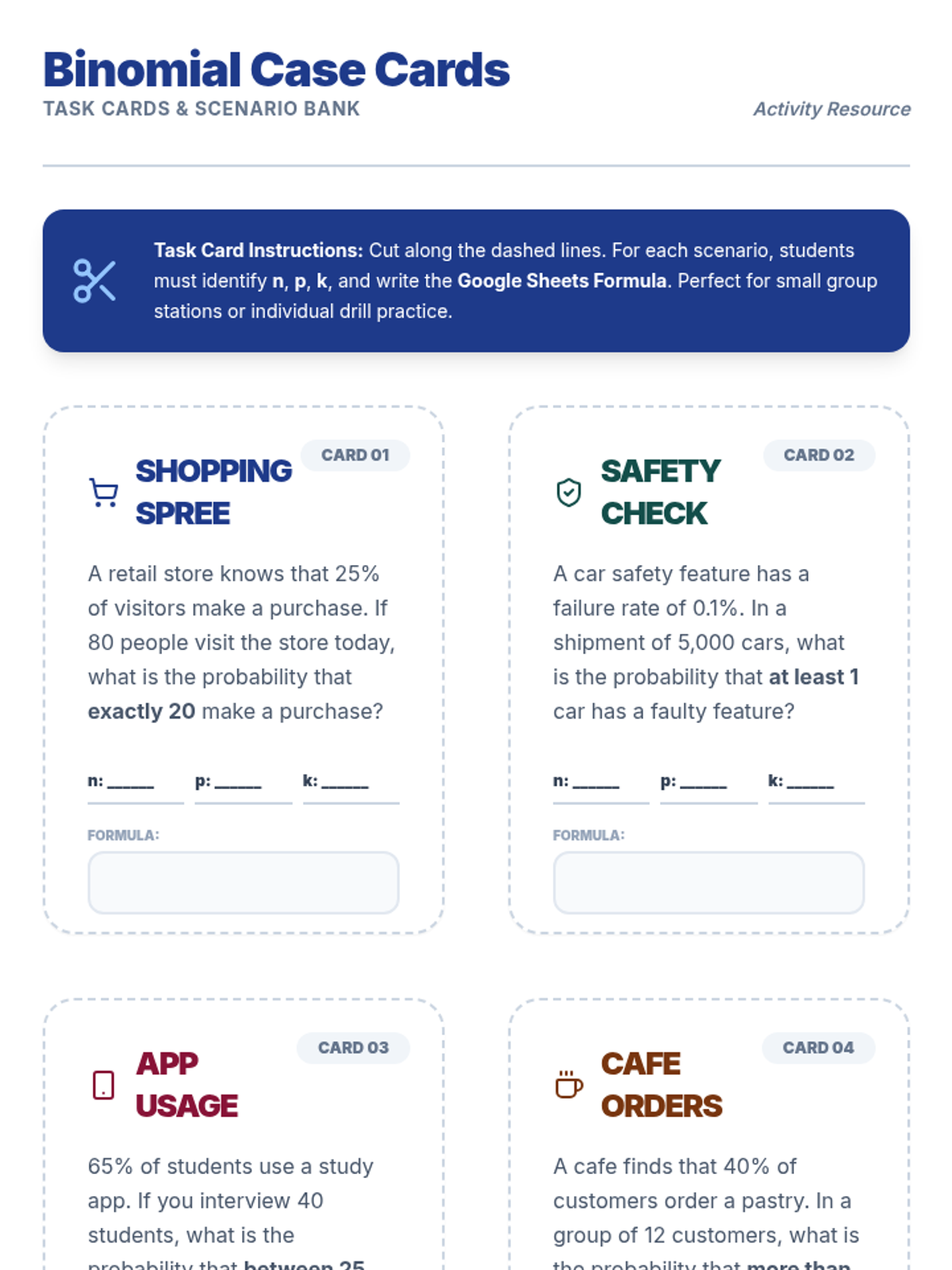

A set of 10 printable task cards featuring diverse binomial distribution scenarios. Perfect for station activities, group work, or extra practice bank. Includes integrated answer key. Now updated to include Expected Value (E[X]) calculations for every case.

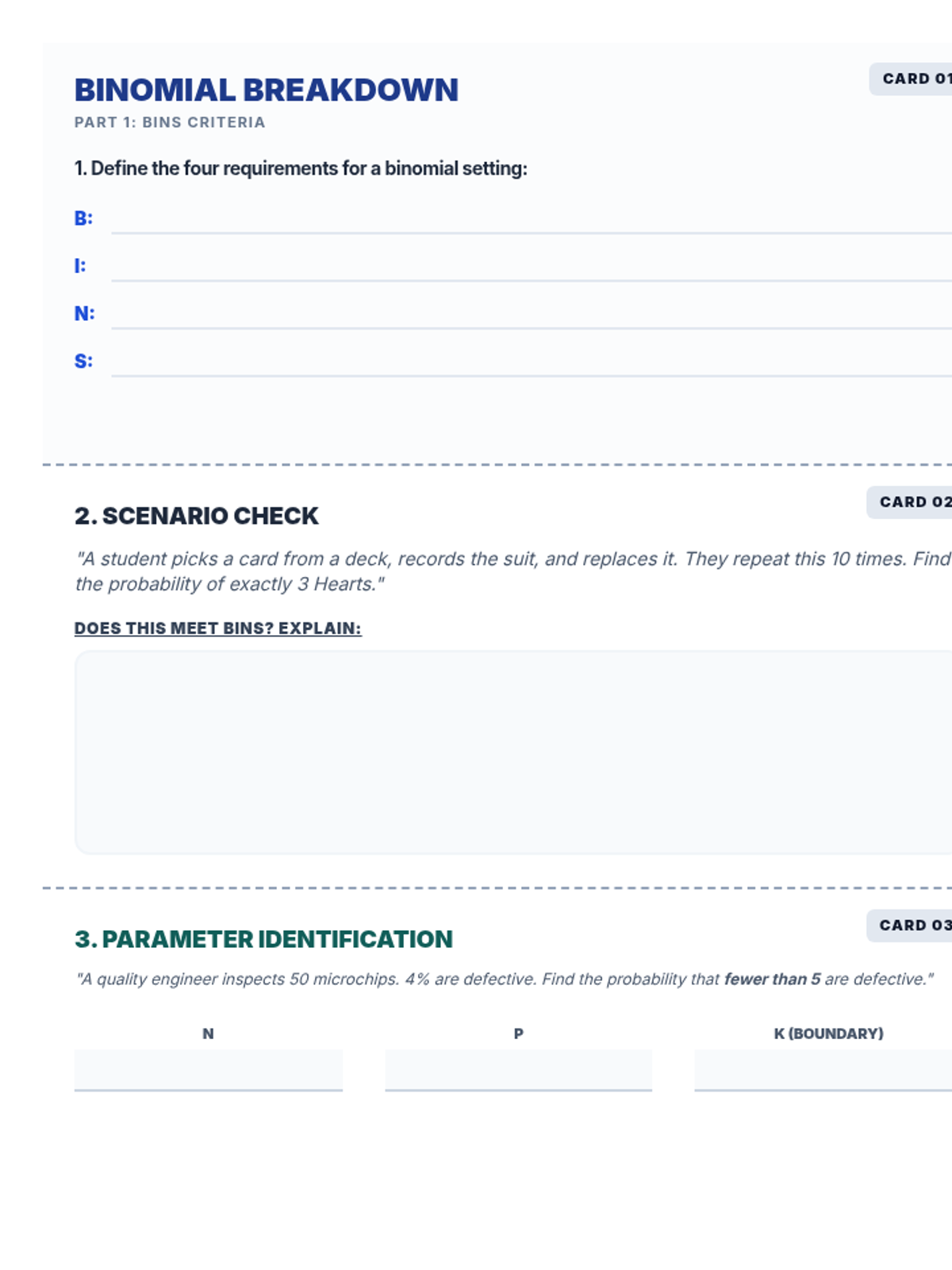

A comprehensive answer key for the task-card edition of the Binomial Breakdown Worksheet, reformatted into individual 1/3-page cards to facilitate separate distribution or physical cutting. Each card provides detailed logic, modern BINOM.DIST syntax, and correctly rendered manual formulas. Updated for density and usability.

A 21-question practice worksheet for 12th-grade statistics, reformatted as a modular task-card bank. Designed with three horizontal cut-lines per page for easy physical division. Covers BINS criteria, spreadsheet formulas (BINOM.DIST), hand-calculation theory, and now includes questions on Expected Value (n*p). Card IDs and questions are aligned 1:1.

A visual presentation accompanying the Binomial Breakdown lesson. Covers BINS criteria, expected value (mean), spreadsheet formula syntax (BINOM.DIST), and the hand-calculation formula connection. Updated with a new slide for expected value (n*p) and improved summary visuals.

A set of 10 printable task cards featuring diverse binomial distribution scenarios. Perfect for station activities, group work, or extra practice bank. Includes integrated answer key.

A visual presentation accompanying the Binomial Breakdown lesson. Covers BINS criteria, spreadsheet formula syntax (BINOM.DIST), and the hand-calculation formula connection. Updated with reliable manual math rendering, corrected tracking, and improved layout stability. Includes a dedicated fill-in-the-blank practice slide.